Latest housing starts data is good for mortgage rates

How are today’s better-than-expected housing starts data good for mortgage rates? Typically, good economic data is bad for interest rates, especially in this environment when a Fed member will say that building or buying houses is bad for fighting inflation. The answer is simple: the best way to fight inflation over the long term is to add more supply.

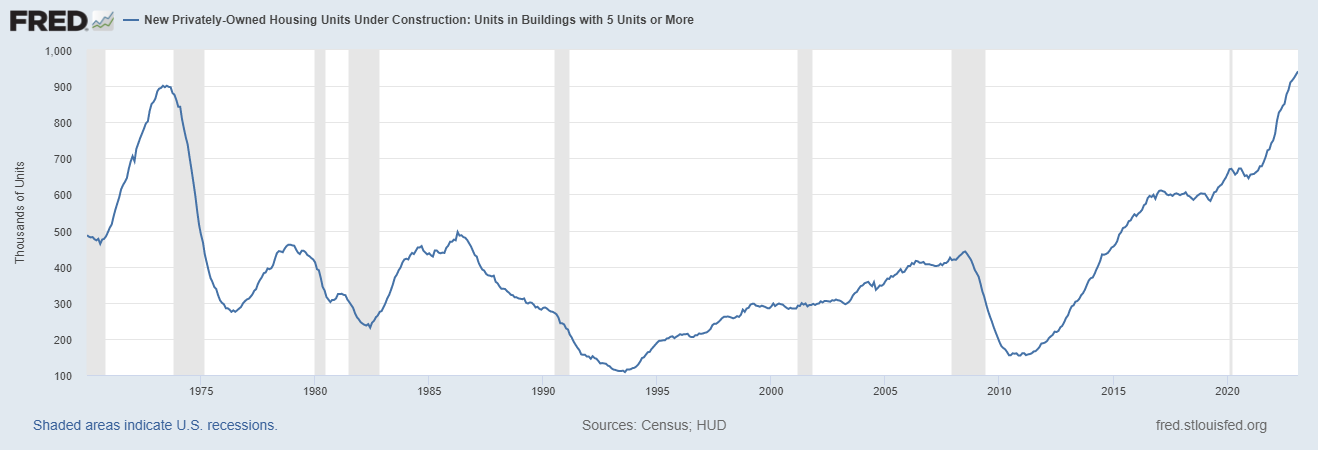

Destroying demand is a short-term solution, but longer-term supply is the natural economic route. What we are seeing in this latest launch report is encouraging as a record 5 units are still under construction and anything that is completed is positive against inflation.

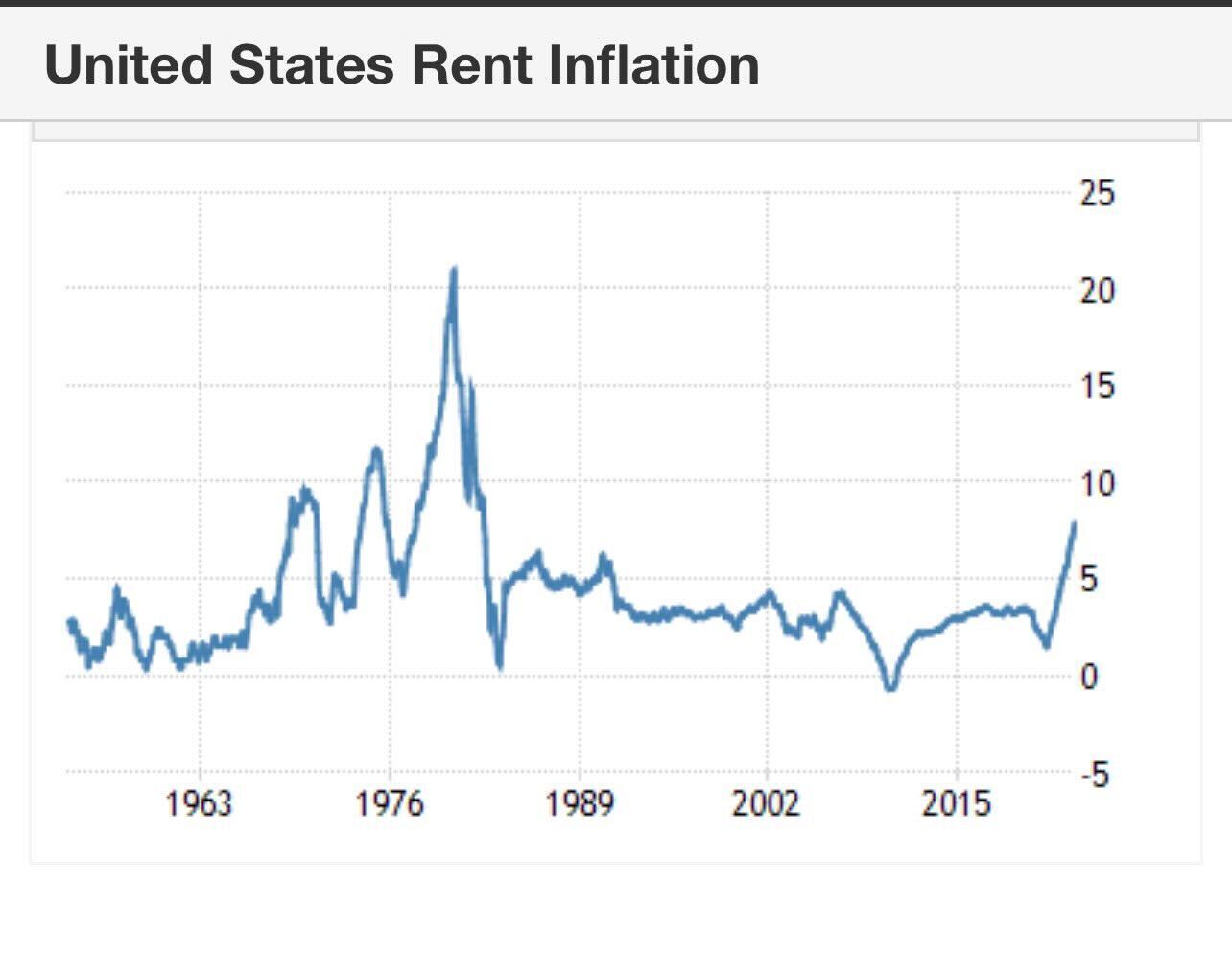

As you can see, the 1974 recession devastated 5-unit build production. As with most recessions, production falls when demand falls. Unlike the 1970s when we had a boom in rents, which make up a whopping 44.4% of CPI inflation data, we now have supply online.

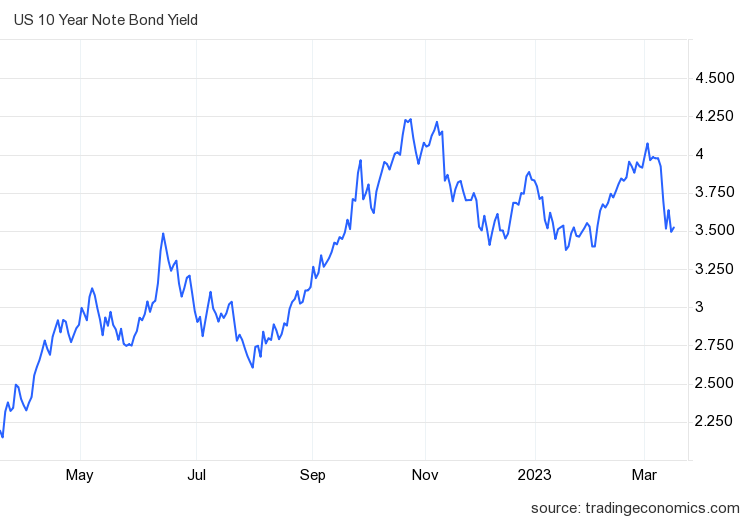

I often talk about how today’s economy is nothing like it was in the 1970’s and the bond market never really believed it either, which is why the 10-year yield today is under 3.50%.

In terms of mortgage rates and bonds, bond yields have been down since the banking crisis began with a run on Silicon Valley Bank last week and are now testing my Gandalf line in the sand of 3.42%.

If the 10-year yield closes below 3.42%, we’ll see more bond buying in the days after that key level breaks, and I’ll be more comfortable with mortgage rates falling. However, it was a struggle to get below that level. As you can see in the chart below, the nice slow dance between the bond market and mortgage rates has been happening since 1971.

My forecast for 2023 quantifies the range for the 10-year return 3.21% – 4.25%which does ______________ mean 5.75%-7.25% mortgage rates. As unemployment claims rise, meaning more people are filing for unemployment benefits, mortgage rates and bond yields will fall.

That’s not happening right now. Jobless claims and housing starts were good both today and on the day Atlanta Fed showed GDP growth of 3.2% for the quarter.

However, the bond market is looking ahead, and the banking crisis here and around the world is sending money into the bond market for the time being. We also need to remember that Wall Street has been severely tight on bonds, which means it makes money when bond yields and mortgage rates rise.

However, since the crisis began, they have had to cover their bets and invest more money than usual in buying bonds. This may explain some of the wild action in the bond market over the past few days.

Earlier Thursday morning the 10-year yield was 3.42%, but as of this writing it is 3.52%. We shall see how mortgage rates are valued in such a wild market.

Report on the start of construction

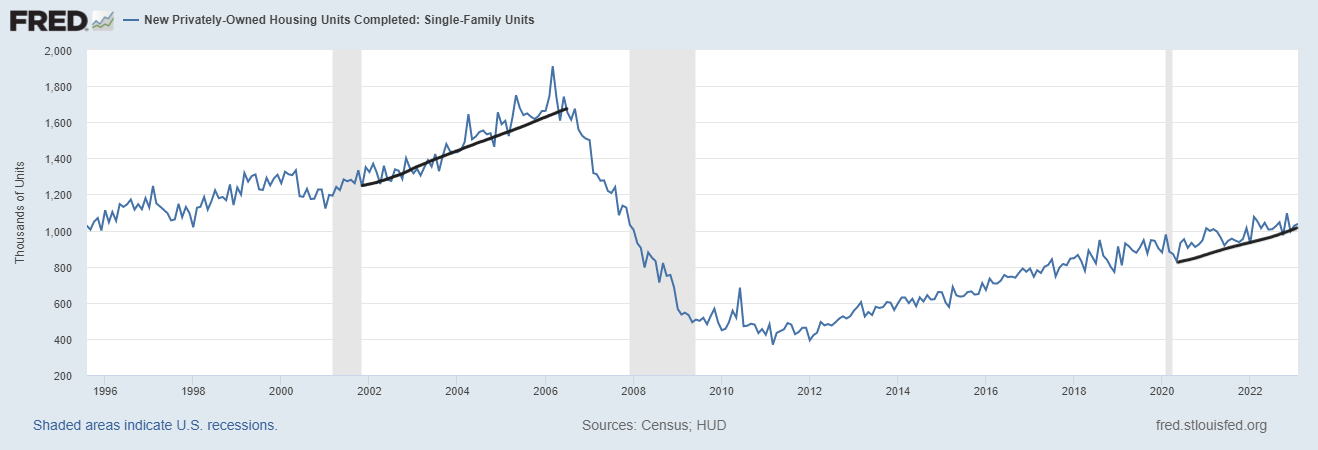

Out of census: Home Completions Completions of privately owned homes were at a seasonally adjusted annualized rate of 1,557,000 in February. This is 12.2 percent (±15.0 percent)* above the revised January estimate of 1,388,000 and 12.8 percent (±16.2 percent)* above the February 2022 rate of 1,380,000. 1,037,000 single-family homes were completed in February; this is 1.0 percent (±15.0 percent)* above the revised January rate of 1,027,000. The February rate for units in buildings of five units or more was 509,000.

As you can see, the apartment completion dates have been a trotting tortoise. The COVID-19 delay in production means we have a backlog of homes to be completed, although more for the 5 unit space than single family homes. The COVID-19 delays have served as an employment program here in America as workers are still needed to finish the backlog of homes.

Many single-family home contracts would not have started if mortgage rates were 6% to 7% on the day of signing. With interest rates soaring so fast, builders are working off that backlog today. Traditionally, completions with permits would fall, but that is not the case today due to the COVID-19 delays.

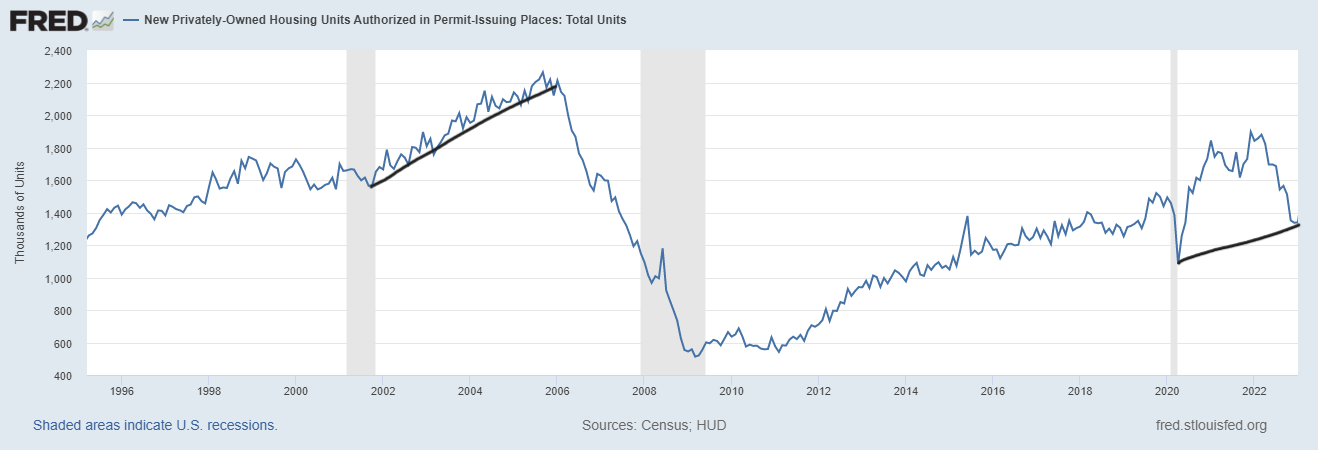

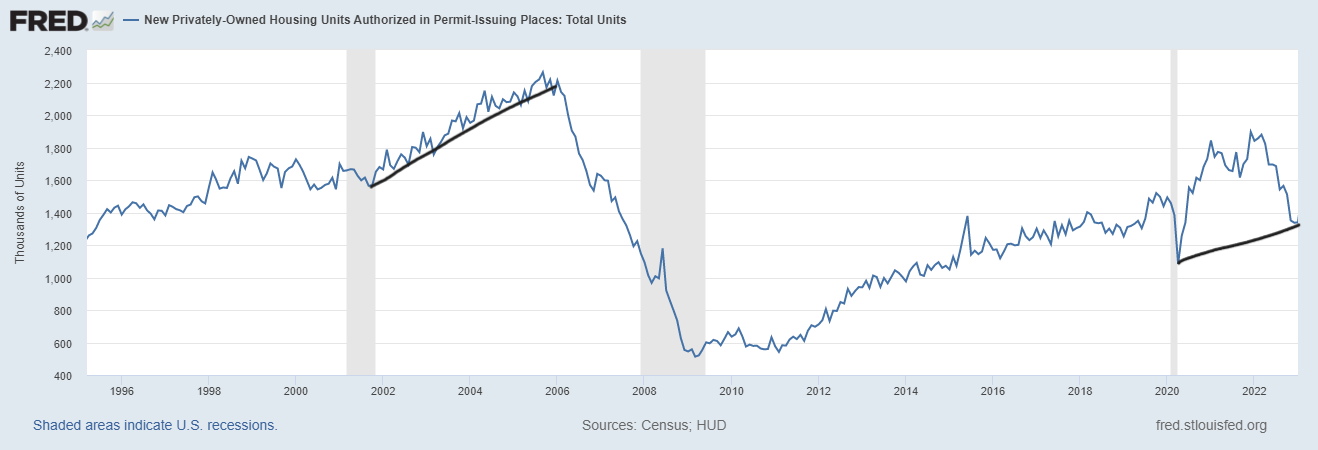

From the census: Building Permits The number of privately owned housing units approved by building permits in February amounted to 1,524,000 a year, seasonally adjusted. This is 13.8 percent above the revised January rate of 1,339,000 but 17.9 percent below the February 2022 rate of 1,857,000. Single-Family Home Approvals were 777,000 in February; that’s 7.6 percent more than the revised January figure of 722,000. Unit permits in buildings of five units or more were 700,000 in February.

The decline in housing permits has continued throughout this report, but the trend is still your friend here as I don’t expect any significant recovery in housing permits until the stock of homes is sold. As you can see in the chart below, today’s data looks different than the massive 2005 surge and collapse.

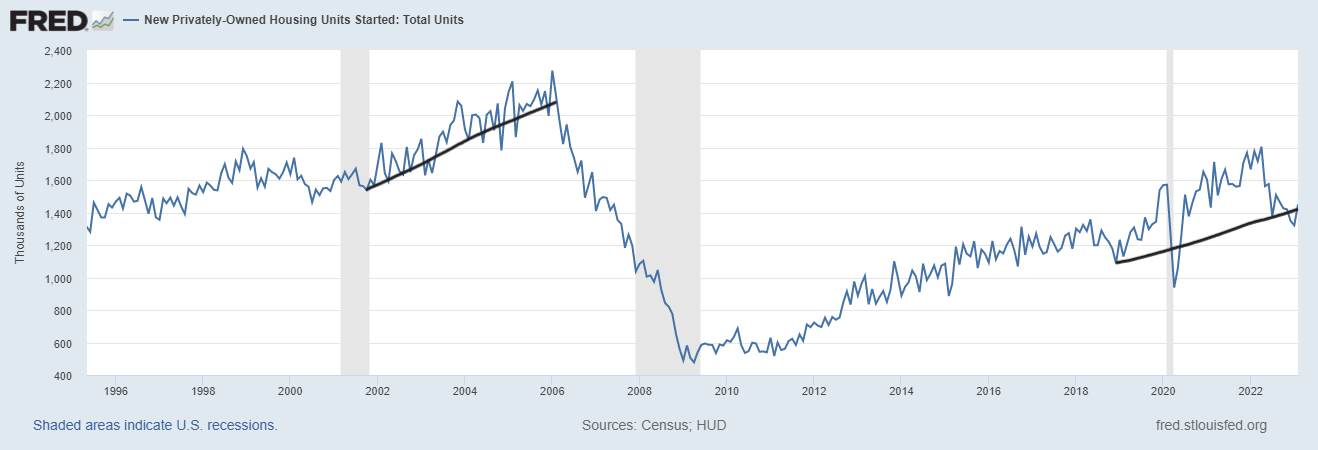

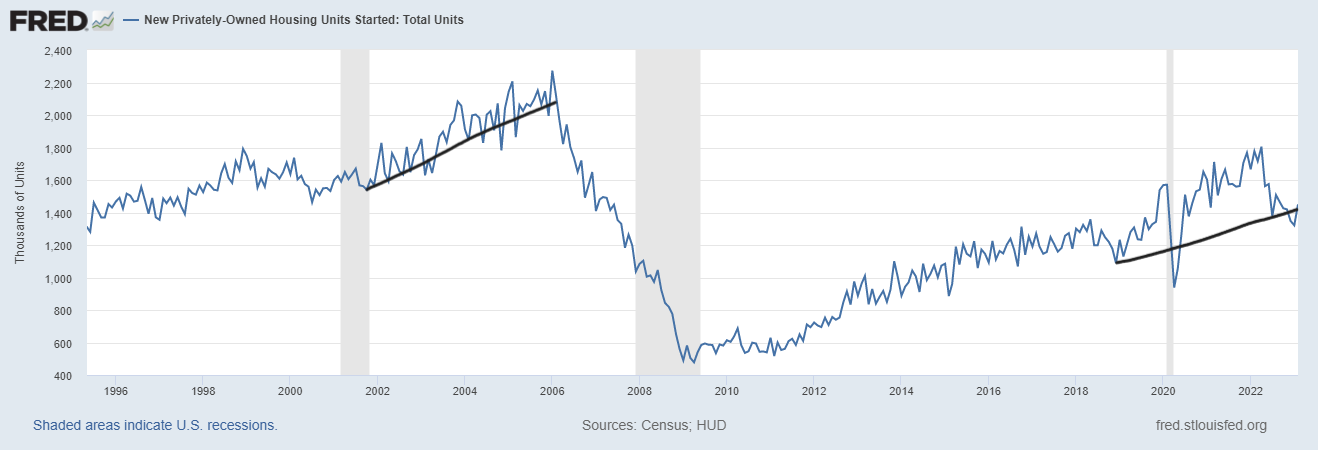

From the census: Housing Starts Private housing starts were at a seasonally adjusted annual rate of 1,450,000 in February. This is 9.8 percent (±15.5 percent)* above the revised January estimate of 1,321,000, but 18.4 percent (±8.9 percent) below the February 2022 rate of 1,777,000. Single-family housing starts in February were 830,000; that’s 1.1 percent (±13.9 percent)* more than the revised January figure of 821,000. The February rate for units in buildings of five units or more was 608,000.

The housing starts data itself is on the up today and as always when it comes to housing starts and new home sales data we have to look back at the revisions that were negative in this report. However, recent new home sales data has improved along with homebuilder confidence.

Overall, I like the report because it still shows that we will get more housing offers. The future growth of 5 unit construction will be at risk if a recession hits. However, the key is that we have more supply, which is the best way to fight inflation.

My rule of thumb for anticipating builder behavior is based on the three-month bid average. This has nothing to do with the existing home sales market; These monthly listing dates are for the new home sales market and current only 7.9 months are too high to be able to issue new permits.

- When supply is 4.3 months and under this is an excellent market for builders.

- When supply is 4.4 to 6.4 months this is an OK market for builders. They will continue to build as long as new home sales grow.

- The builders will withdraw construction when supplies last 6.5 months and above.

As you can see below, in the last new home sales report, the monthly listing data fell from 9 months to 7.9 months so we still have a lot of work to do here to get things back to normal.

On a positive note, builders are feeling a little more perky these days. Of course we are working on a waterfall jump in demand, but it is still positive that builder confidence has increased.

Confidence index for builders

This week’s housing starts and homebuilder confidence report is positive for the future of mortgage rates. We see that inflation is being fought in the right way with supply and lower mortgage rates, meaning future housing production could be better than some thought once the arrears are cleared.