By James Smith, Developed Markets Economist; Chris Turner, Global Head of Markets and Regional Head of Research for UK & CEE and Francesco Pesole, FX Strategist

The Global Risk Environment and Potential Narrowing Interest rate differentials between the UK and the eurozone are likely to prove a more important driver of sterling than the new UK-EU deal. We prefer the EURGBP to find support in the 0.87/0.88 area and end the year closer to 0.89/0.90.

Windsor Framework makes life easier for companies trading with Northern Ireland

The UK and EU have finally agreed on an agreement that will make life easier for companies trading between Great Britain and Northern Ireland (NI).

Recall that a key objective of the original Brexit deal, signed by then Prime Minister Boris Johnson in 2019, was to keep an open border within the island of Ireland. The This solution effectively kept NI in the EU single market for goods and thus required customs and food documents for shipments traveling from mainland UK via the Irish Sea.

The new “Windsor Framework” agreed this week is intended to remove many of the major frictions that arose from that original deal. The new framework introduces systems for trusted traders and green/red lanes in ports, while addressing specific contentious issues such as chilled meat exports – making various grace periods that have been successively extended since 2021 permanent.

But while all of this is undoubtedly a welcome move – and underscores a healthier relationship between London and Brussels – the economic impact on the UK economy as a whole will likely be negligible.

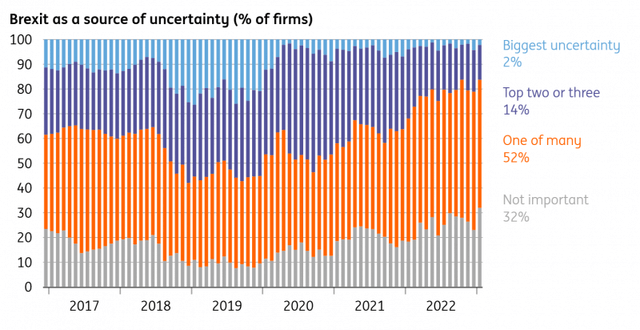

Brexit is no longer a key uncertainty for companies

Bank of England

The new deal doesn’t improve trading conditions between the UK and the EU – nor is it likely to boost investment

In part this is simply because Northern Ireland accounts for only around 2% of UK economic output and Northern Ireland’s economic growth has tended to be faster than that of the UK as a whole in recent years. There is no compelling evidence that issues related to the NI Protocol have negatively impacted overall UK activity.

Instead, we must ask ourselves two questions:

First, will the Windsor framework herald a broader improvement in UK-EU trade relations? Last but not least, it effectively removes the tail risk of the EU suspending the entire free trade agreement, something that had been a remote possibility when relations among previous UK leaders had deteriorated. Healthier relationships also open the door for future deals in other areas, and indeed this week’s deal opens the door for the UK’s re-entry into Horizon, the EU’s science programme.

However, such mini-deals are unlikely to create material differences in the overall trading environment between the UK and the EU. There is little prospect of the UK re-entering the single market or customs union, and the outcome of the next general election (due until January 2025) is unlikely to change that. Labour, currently leading the polls, is signaling he is unlikely to seek sweeping changes in Brussels.

The additional trade barriers created by the UK-EU Free Trade Agreement helped UK exports to underperform during the pandemic. The UK has missed out on the 2020/21 global trade recovery, although admittedly the data has been looking a little better of late thanks to strong services exports last year.

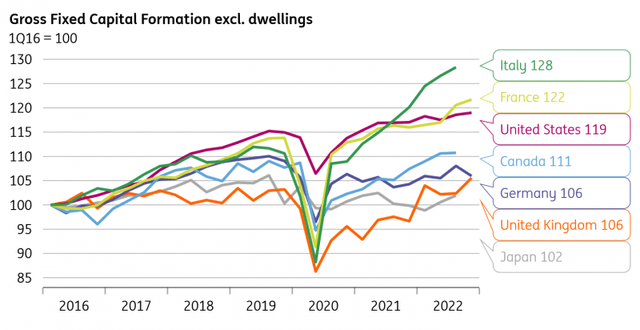

The second question we need to ask is whether the new deal will boost investment. Brexit uncertainty has undoubtedly contributed to the underperformance of UK investment since the 2016 referendum. The level of non-residential investments has fallen noticeably below the USA, Italy and France (but less so Germany).

In reality, while more clarity on EU relations is helpful, Brexit is no longer a major source of uncertainty for businesses. While half of businesses saw Brexit as one of the top three sources of uncertainty in 2019, it is now just one in six, according to Bank of England survey data (chart above).

Instead, it’s the broader economic environment — and the outlook for energy prices — that will be the primary driver of investment over the coming quarters. Investment intentions rebounded in late 2021 following the pandemic but have since declined.

The UK has underperformed on investment

Macrobond, ING calculations

Calculated on the basis of data from the OECD National Accounts and excluding investment in residential real estate from total gross fixed capital formation

GBP: Welcome news, but not a game changer

Sterling has fared slightly better in recent sessions, gaining about 0.7% against the euro – its main benchmark in Europe. Sterling’s move was slightly larger against the dollar, although here GBP/USD appears to be riding on the back of stronger EUR/USD following the release of high Spanish and French February inflation data on the 28th.

As James explains above, it is unlikely that this Windsor agreement will fundamentally alter the UK’s growth prospects. The question, however, is whether the prospect of improved political ties with Brussels reduces some kind of hard Brexit risk premium embedded in the pound.

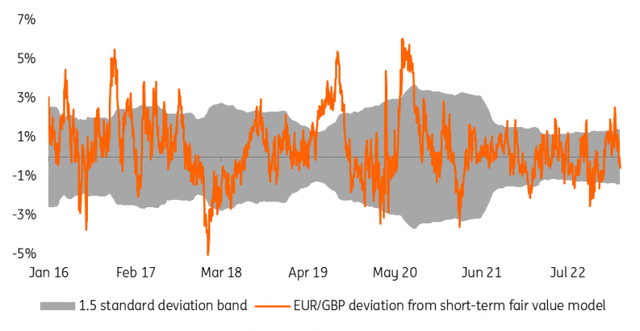

Trying to quantify a risk premium in the currency markets is always difficult. In the past we’ve used our Financial Fair Value (FFV) models to figure out where FX pairs should trade on historical relationships – and then identified any deviations as some sort of risk premium.

Included in this FFV model are market drivers such as short-term interest rate differentials, relative and global stock performance, and the shape of yield curves. As our chart below shows, there have been times – such as during the Brexit Deal discussions in 2019 and in the early stages of the pandemic – when the GBP has traded with a 5% risk premium. In other words, EUR/GBP traded 5% above the levels suggested by the FFV model.

Estimation of the financial fair value of EUR/GBP by ING

ING

More recently, however, EURGBP has traded in line with short-term financial variables and the hint of a hard Brexit tail risk (ie a full collapse in UK-EU trade relations post-Brexit) has not really been present in sterling . This suggests that this new arrangement may not require a significant rally in sterling.

Instead, we expect Sterling to be driven this year by a combination of relative growth/monetary outlook and the overall risk environment. This latter factor remains a key driver of sterling given the UK’s large twin deficits and the relatively large size of the financial sector in the UK economy.

what is the view It seems pretty clear that interest rate differentials between the Eurozone and the UK will narrow as the European Central Bank catches up with the Bank of England’s previous tightening cycle. At the same time, the global risk environment remains subdued as persistent inflation forces central banks to tighten in recessions.

We prefer the EURGBP to find support in the 0.87/0.88 area and end the year closer to 0.89/0.90. GBP/USD is a different story where we continue to wait for Federal Reserve easing by the end of the year and a weaker dollar. Our base view is for GBP/USD to find support below 1.20 in this first quarter and manage to trade in a 1.25 to 1.30 range by the end of the year.

Content Disclaimer

This publication has been prepared by ING for informational purposes only, regardless of the means, financial situation or investment objectives of a specific user. The information does not constitute an investment recommendation, investment, legal or tax advice, or an offer or solicitation to buy or sell any financial instrument. Read more.

Original post

Editor’s note: The summary points for this article were selected by Seeking Alpha editors.